Let’s say you’re considering bankruptcy and are interested in understanding whether you qualify for a free pre-bankruptcy credit counseling course as defined by the US government.

Firstly, the calculator below uses questions from the definition to estimate whether you can qualify for free credit counseling course.

In addition, I’ll include a snippet from them below:

Your next question may be: “What are the poverty guidelines for your state, and how is household income calculated?”

Poverty guidelines change, and it can be challenging to understand how your annual household income can be calculated, so make sure to understand the updated figures.

What Are My Next Steps To See If I Qualify?

1. Choose an approved credit counseling agency

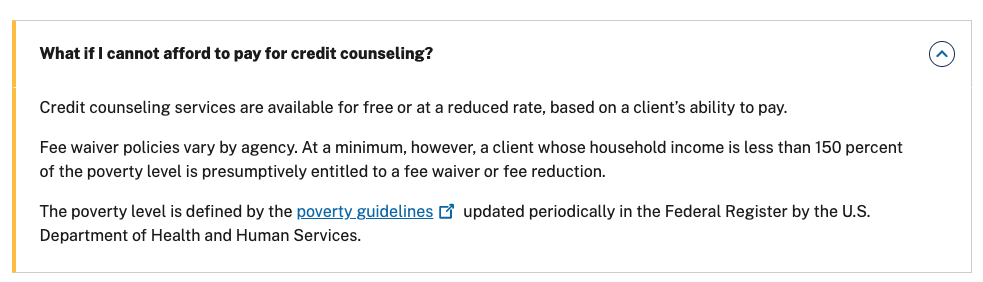

All credit counseling and debtor education course providers approved by the U.S. Trustee Program (USTP) are required to offer services free or at a reduced rate based on a person’s ability to pay (source).

The above calculator already understands which state and which are approved, but if it’s helpful, please see the list of approved credit counseling course providers in your state:

1. Alabama and North Carolina: Approved provider list

2. All Other states: Approved provider list

Once you select an agency, check out step #2.

2. Fill out the fee waiver before starting the course

Once you select an agency, you will want to request their fee waiver process. This can include the agency asking for your proof of income and household size.

You may have to provide the following information:

- Recent pay stubs, W-2s, or tax returns

- Social security, unemployment or disability benefit letters (if applicable)

- Documents showing household size, such as the latest tax return or dependent claims.

Each agency may have slightly different requirements, so it may be best to check its disclosures page before applying.

3. Complete the course and get a certificate

Once your fee waiver has been approved, then you may start the course. Please note, it may be difficult to get a refund if you’ve already paid for the course.

For the fee waiver, you may get a waiver code or written confirmation that the fee has been waived.

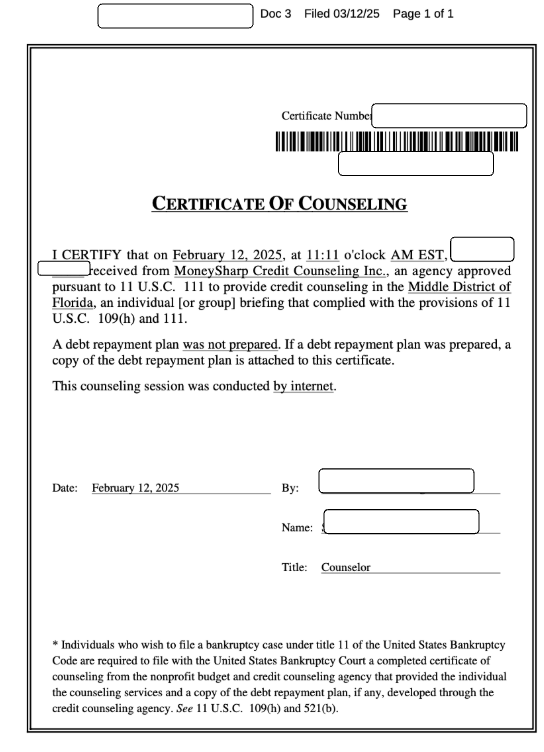

Once you’ve taken and completed the course, you may receive a certificate of completion which is the required document to file with your bankruptcy petition. Here’s an example of an actual redacted copy of a certificate of credit counseling.

Pre-Bankruptcy Course Caveats

If you are unable to qualify for a free pre-bankruptcy credit counseling course, please be aware of the following as you look for the cheapest US government-approved credit counseling courses.

1. Understand Up Charges Before Purchase

When I was researching pre-bankruptcy credit counseling courses, I was alarmed that non-profit organizations were actually upcharging for their services.

For example, I believe one company actually upcharges for a similar online certificate fee or video course fee, which is a bit shocking, as it didn’t seem to provide any other option than to be upcharged.

When the total bill came, the course appeared to be around $50.00, even though the marketing made it seem that the course was between $15-$25, if I remember correctly.

In the calculator above, I tried to account for that by providing only the cheapest courses with the cheapest all-in fee.

2. Understand How The Course Is Offered

Some non-profits may only offer a telephone option, while others may only offer an online course option.

There are generally four different ways you can take the pre-bankruptcy credit counseling course, including:

- Online – These are often self-paced via a web portal that is available 24/7. In addition, you can often instantly get your certificate after completion.

- Phone – These are often counselor-led over the phone. You may need to schedule a call, and the certificate could be issued after the call.

- In-Person – Offered at a local agency’s office. This may be the least preferred option, and you might get it after you end the session.

- Mail/Paper – The mail and paper option would be where you fill out a packet and return it via mail. This would be a minimal option, and you’d get your certificate after the counselor’s review.

If your preference is an online course, confirm that the credit counseling course provider you are considering offers that option.

3. Understand State Requirements

Alabama and North Carolina are unique in that they have a separate website listing the approved credit counseling and debtor education course providers.

The above calculator already understands which state and which are approved, but if it’s helpful, please see the list of approved credit counseling course providers in your state:

1. Alabama and North Carolina: Approved provider list

2. All Other states: Approved provider list

Once you are done with the course, make sure you get your certificate, which you can utilize in your bankruptcy petition packet.

Conclusion

Hopefully, you have a better understanding of whether you qualify for a free pre-bankruptcy credit counseling course and, if not, which pre-bankruptcy course is the cheapest.

In addition, you now have an understanding of whether a non-profit credit counseling course may upcharge you for certain features, how the course can be offered, and also requirements for states such as North Carolina and Alabama.